The announcement of new cooling measures didn’t shock us as much, for at some point we are watching it to happen.

Those that are watching the property market saw that the new cooling measures are coming but it’s just a matter of when and how much impact it will have.

As a busy professional & home owner, you may have a lot of questions about how these new cooling measures affect you. Here, we will help you understand how each measure affects you and what you can do about it.

To give you a quick recap, here’s the breakdown of the new cooling measures announced by MND (Ministry of National Development).

- Higher ABSD

- Lower TDSR

- Reduced LTV (Loan-to-value) limit for HDB loans

MEASURES TO COOL THE PROPERTY MARKET

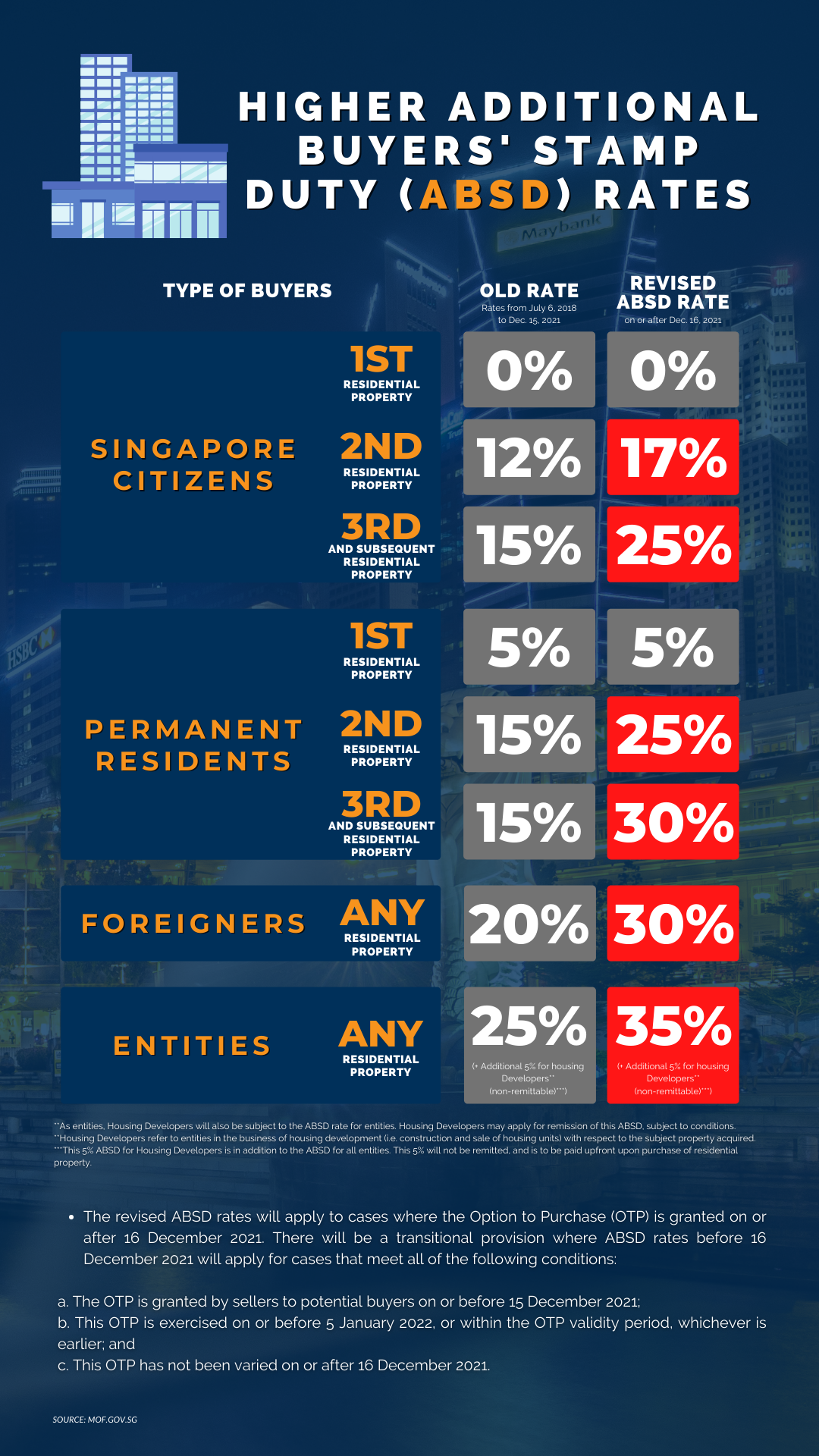

ADDITIONAL BUYER STAMP DUTY (ABSD)

First in the list of the new cooling measure that the government imposed is the Additional Buyer Stamp Duty or ABSD. ABSD is a TAX you pay for property. The amount you pay for ABSD is based on your citizenship status and the number of properties you currently have.

Singapore Citizens they will now pay the new ABSD of 17% for their 2nd property and 25% ABSD for their 3rd and subsequent residential property as opposed to previous rates of 12% & 15%.

PRs will now pay the new ABSD of 25% for their 2nd property and 30% ABSD for their 3rd and subsequent residential property as opposed to previous rates of both 15%.

Foreigners buying any residential property in Singapore, their ABSD is now 30% from 20% previous rate.

Entities, Corporations and housing developers, their ABSD now is 35% plus an additional of non-remittable 5%. This adds to the pressure on them to complete and sell all units within the 5-year deadline if they want to remit the 35% ABSD.

LOWER TDSR (TOTAL DEBT SERVICING RATIO)

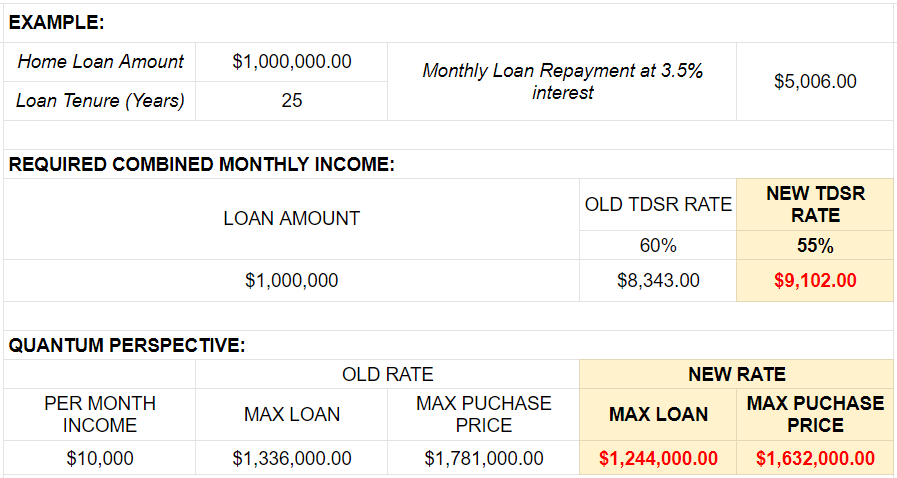

The NEW Total Debt Servicing Ratio or TDSR has been reduced by 5%. It’s even better because it will make homebuyers have a reality check, whether or not they are over-leveraging themselves when buying property.

Home buyers need to remember that TDSR consists of not only their monthly mortgage but also other debt obligations like car loans, credit cards etc.

So it’s wise to review any debt commitment you currently have to see which one can be eliminated first before buying property because financial planning is a BIG FACTOR when buying a property.

You don’t want to put yourself in a position where you are struggling to pay your monthly mortgage along with other obligations you have.

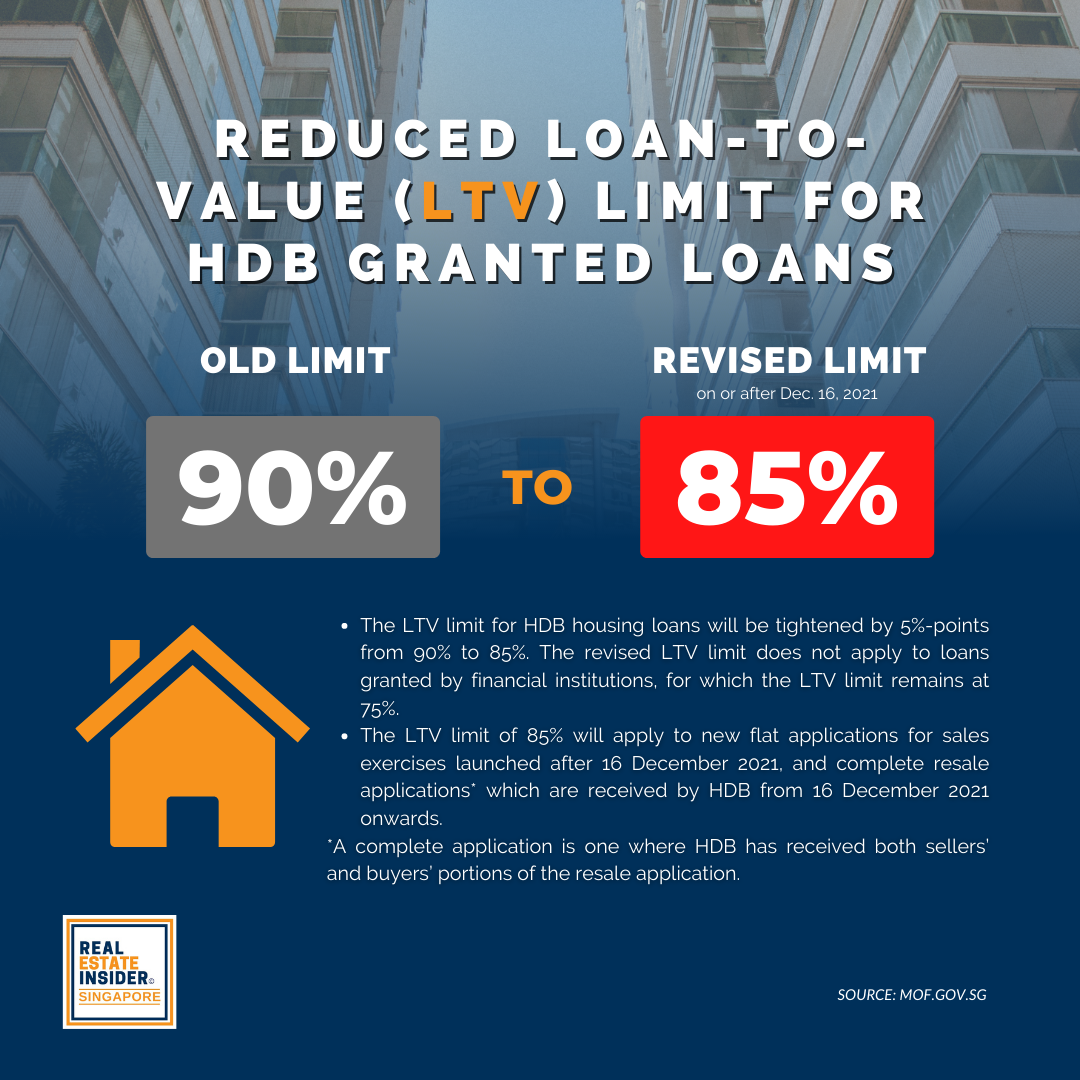

NEW COOLING MEASURES TO REDUCED LOAN-TO-VALUE LIMIT FOR HDB LOANS

For HDB buyers, bear in mind that the reduced LTV limit means you will now need to pay a higher deposit, from 10% before, it has increased to 15% deposit.

The revised limit reduces the amount potential homebuyers can borrow from HDB. LTV Limit for loans obtained from financial institutions to purchase HDB flats remains unchanged at 75%. No change to LTV for those on a bank loan.

The LTV change is not much of a big issue for homebuyers actually.

WHAT YOU CAN DO ABOUT THE NEW COOLING MEASURES AS A HOME OWNER

Now that you have an overview of what the new cooling measures are, you may be thinking, how can this affect me as a home buyer, and is it possible to avoid these changes?

Let’s break down the effects per home buyer profile. How does the change affect the:

- First-time Buyers

- HDB Upgraders

- Foreigners

- Entities and Developers

THE COOLING MEASURES AND THE FIRST-TIME BUYERS

Since ABSD change applies to the 2nd property purchased and the subsequent ones, this doesn’t affect first-time buyers particularly. The only thing that could affect you is the LTV or Loan to Value which means higher down payment for you and the tighter TDSR (Total Debt Servicing Ratio).

As first-time homebuyers, the new TDSR affects you by LOWERING YOUR PURCHASING POWER. But of course you can adjust your finances, make bigger Down Payments and borrow less until the TDSR limit fits your purchasing ability.

If reduced TDSR really is an issue for you to buy property, maybe you should check if you are over leveraging yourself and look for a property that’s within your means instead.

Are there ways to increase this limitation? There are ways to properly structure your financials but we will not cover them here. Reach out to us if you like to explore more in detail.

If you are looking HDB as your purchase, the NEW (reduced) LTV for first-time buyers, will only affect you in terms of financing a higher down payment, which will not be felt much since you can have your CPF cover for it.

When you buy HDB flat, you can only set aside up to $20,000 in your CPF Ordinary Account (OA). The remaining balance will be used for the down payment.

For Singaporean couples, their combined OAs means they’ll make a way bigger down payment than the minimum 15% required.

For example, an HDB resale flat with a valuation of $500,000 would require a minimum down payment of $75,000 (15% of $500,000), up from $50,000 previously.

HDB UPGRADERS AFFECTED BY TIGHTER MEASURES

Let’s start by citing an example.

A Singapore buyer purchasing a private property for $1,000,000 before selling the existing HDB flat (or any other property), with the new cooling measure, he/she will need to pay the following:

New ABSD + BSD + OTP + To exercise the option + DP = Total Cost to pay

New 17% ABSD (Additional Buyer Stamp Duty) = $170,000

BSD (Buyer Stamp Duty) = $24,600

OTP (Option-to-Purchase) 1% = $10,000

To Exercise OTP 4% = $40,000

TOTAL : $244,000

In total, they will need a cash outlay of at least $244,600 to purchase a $1 million private property. Do note they still need to pay the remaining down payment of $200,000 (20% of $1,000,000) in cash or CPF.

So, $244,400 + Down Payment (20%) = $200,000

TOTAL COST TO PAY = $444,000

In total, you are looking at an upfront cost of $444,600, of which at least $244,600 would need to be paid for using cash.

While the ABSD ($170,000 in our example) can be refunded upon the sale of their existing HDB flat (or any other private property) within 6 months, the point here is that buyers still need to have the cash first to complete the transaction.

Of course, the alternative to avoid ABSD in the first place is to sell our existing property before purchasing our private property.

However, there are also some challenges with that particularly during the pandemic where it could be very inconvenient for families if they need to move out of their existing home without their new place being ready yet.

THE NEW COOLING MEASURE AND FOREIGNERS

If you are a foreigner, 30% ABSD could prove to be a concern for many foreign buyers, especially for big ticket purchases in CCR.

With this preemptive measure, the government has placed this in preparation for foreigners who will be coming to SG to open businesses and looking to buy luxury homes as the borders are now slowly opening.

ENTITIES AND DEVELOPERS

With the high ABSD for developers, and the additional non-remittable 5%, developers need to be more selective in buying their land acquisitions that will in turn affect En Bloc transactions.

This additional hike on ABSD for developers will surely affect future property prices which will be a concern for future buyers. Though they can remit the ABSD if they sell all units within the 5-year period, this will still be challenging for them.

CONCLUSION

New information can scare us when we don’t really know the story behind it. The New cooling measures can be threatening for the uninformed, but can be a strong foundation for those who know how to use this information to their advantage.

With the New rounds of Cooling Measures, we can clearly see that these will have an impact more on Foreigners and developers than for the regular home buyers.

We have to see these new cooling measures as a way for the government to keep property prices in check. With this, Singapore will continue to have stable and affordable property prices even for the next generation of buyers.

We can take this measure and emerge winners in the end. For a more personalized solution to your property situation, We have a private group where we help busy professionals & home owners make 6-figure profits in their property safely. Just click the JOIN button below to be part of the exclusive group to learn the traits and strategy behind it.